Special Festival Advance Scheme which was meant for non-gazetted government employees is being revived as a one-time measure, for gazetted employees too. All central govt. employees can now get interest-free advance of Rs. 10,000, in the form of a prepaid RuPay Card, to be spent by March 31, 2021.

The one-time disbursement of Special Festival Advance Scheme is expected to amount to Rs. 4,000 crore; if given by all state governments, another Rs. 8,000 crore is expected to be disbursed. Employees can spend this on any festival.

Festival advance along with other similar advances were abolished on the recommendations of 7th Pay Commission. It is proposed to restore the Festival Advance to Government employees for festivals up to 31.3.2021

Interest-free advance of Rs. 10,000/- to be recoverable in maximum 10 instalments

Rs. 4,000 crore expected to be disbursed

If given by all State Governments, another Rs. 8000 crores is likely to be disbursed; assuming 50% adoption by states estimate is Rs. 4000 crores

No permanent increase in government expenditure—advance will be recovered

Additional consumer demand generated will be Rs. 8,000 crore.

Employees will get pre-loaded Rupay Card of the advance value.

Government will bear Bank charges in this regard

Ensures digital mode of payment, resulting in tax revenue and encouraging honest businesses

Under LTC Cash Voucher Scheme, government employees can opt to receive cash amounting to leave encashment + 3 times ticket fare, to buy something of their choice. The items bought should be those attracting GST of 12% or more. Only digital transactions are allowed, GST Invoice to be produced.

The biggest incentive for employees to avail the LTC Cash Voucher Scheme is that in a four-year block ending in 2021, the LTC not availed will lapse, instead, this will encourage employees to avail of this facility to buy goods which can help their families.

Estimated cost of LTC Cash Voucher Scheme: For Central govt. : ₹ 5,675 crore; for PSBs & PSUs: ₹ 1,900 crore.

Tax concessions for LTC tickets available for state govt. & private sector too, if they choose to give such facility, these employees too can benefit

Indications are that savings of govt. and organized sector employees have increased, we want to incentivize such people to boost demand for the benefit of the less fortunate. On a conservative basis, we expect the LTC Cash Voucher Scheme to generate additional consumer demand in the range of ₹ 28,000 crore.

– Union Finance Minister Smt. Nirmala Sitharaman

Leave Travel Concession (LTC) Cash Voucher scheme

Central Government Employees get LTC in a block of 4 years (one to anywhere in India & one hometown or two for home town)

Air or rail fare, as per pay scale / entitlement, is reimbursed and in addition, Leave encashment of 10 days (pay + DA) is paid

Due to Covid-19, employees are not in a position to avail of LTC in the current block of 2018-21

In lieu of one LTC during 2018-21, cash payment will be made :

Full payment on Leave encahment and

Payment of fare in 3 flat-rate slabs depending on class of entitlement

Fare payment will be tax free

An Employee, opting for this scheme, will be required to

Buy goods / services worth 3 times the fare and 1 time the leave encashment

Do so before 31st March 2021

Money must be spent on

goods attracting GST of 12% or more from a GST registered vendor

throught digital mode

GST invoice will be required to be produced

Financial Boost to the Economy

If Central Government employees opt for it, cost will be around Rs.5,675 crore. Employees of PSBs and PSUs will also be allowed this facility and the estimated cost for them will be Rs. 1,900 crore.

The tax concession will be allowed for State Government/Private sector too, for employees who currently are entitled to LTC, subject to following the guidelines of the Central Government scheme

Demand infusion in the economy by Central Government and Central PSE/PSB employees is estimated to be Rs. 19,000 crore approx. Demand infusion by State Government employees will be Rs. 9,000 crore.

Additional consumer demand generated will be Rs. 28,000 crore

Finance Minister Nirmala Sitharaman today addressed the media on key economic issues. The following schemes are announced for Central Government Employees in this meeting :

The interest-free advance of Rs 10,000 under the Special Festival Advance Scheme to be paid back in 10 instalments.

The one-time disbursement of Special Festival Advance Scheme is expected to amount to ₹4,000 crore; if given by all state governments, another ₹8,000 crores is expected to be disbursed. Employees can spend this on any festival.

Special Festival Advance Scheme for non-gazetted employees is being revived as a one-time measure, for gazetted employees too. All central govt. employees can now get an interest-free advance of Rs.10,000, in the form of a prepaid RuPay Card, to be spent by March 31, 2021

Special Festival Advance Scheme is being revived as a one-time measure. All central govt. employees can now get interest-free advance of Rs. 10,000, recoverable in maximum 10 installments: Finance Minister

Employees will get pre-loaded Rupay Card of the advance value

Under LTC Cash Voucher Scheme, government employees can opt to receive cash amounting to leave encashment plus 3 times the ticket fare, to buy items that attract GST of 12% or more. Only digital transactions allowed, GST invoice to be produced, said Sitharaman.

The Secretary,

Government of India,

Department of Personnel & Training,

North Block,

New Delhi

Dear Sir,

Sub : Computation of gratuity and leave encashment in the case of persons retired/to be retired after 1.1.2020 Consequent upon the denial of DA/DR

We invite your kind attention to the orders in F. No. 1/1/2020-E II (B) dated 23.04.2020 wherein the decision of the Government to deny the dearness allowance deafness relief to the employees and pensioners respectively has been conveyed. We had written two letters in the matter on 23rd April 2020 and on 26th May 2020. The undersigned had taken up the issue also with the Cabinet Secretary. when he assured of an informal discussion in the matter with the Staff Side. However. no talks have taken place thereafter. It is not for the first time that the Government is by pausing the National Council. Staff Side. On the last occasion. when the National Council met. we had pointed out the inordinate delay in convening the meetings. We are constrained to believe that the Government wanted the negotiating body to have a burial. I am however duty bound to convey the growing resentment of the employees over this unprecedented decision. As the Government has decided to deny the dearness relief to the pensioners. the pensioner community is in great financial stress as many of them are compelled to spend exorbitant amount for the treatment of Covid.

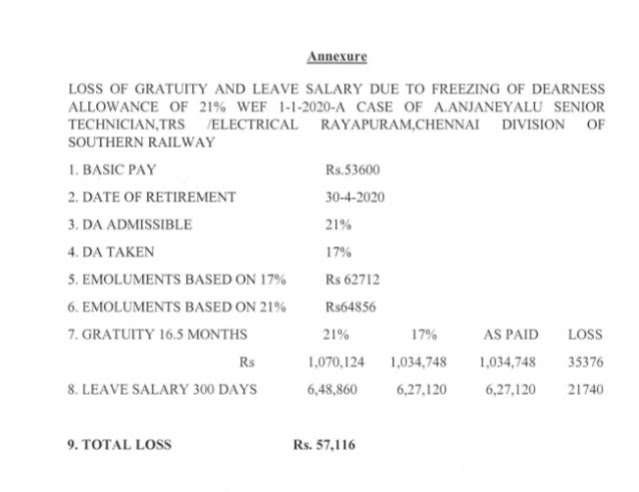

It has been brought to our notice that the denial of DA and freezing the same for Iced 18 months from 1.01.2020 to 1.07.2021 has created a piquant situation for the lower level administrative functionaries to correctly compute the retirement benefits in the case of those civil servants who are retiring after the date of issue of the above cited O.M. The definition of “emoluments” for the purpose of computing the gratuity as also the leave salary (of the accumulated leave) includes Dearness allowance as admissible and not as paid or payable to the Government servant. Without exception. every administrative Department has computed the entitlement on this account only with reference to the Basic pay Dearness allowance paid or received by the concerned individual i.e 17%, Either 21% w.e.f 1-1-2020 or figure increase in percentage are not taken into account while calculating gratuity and leave salary. Since the order of the Finance Ministry clearly stipulates that the Dearness Allowance admissible to the Government servants would be restored on 1.07.2021. the computation of Gratuity and leave salary without taking into account the DA as admissible to the individual Government servant is incorrect. Annexed to this letter is an example as to how the individual loses out if the present faulty, computation procedure is followed It could be seen from the given example, the concerned Government servant will lose a staggering sum of Rs. 57116 because of this faulty computation.

The Government is required to pass the orders as and when the DA has become due, Freezing it for certain period of time or denying it altogether for a specified duration are altogether different issues. Our objection to the adopted policy has already been conveyed to the Government. The faulty computation of Gratuity and Leave salary is not even intended by the order issued by the Government on 23rd April, 2020.

We, therefore. request you to kindly get the matter examined and ensure that

(i) Orders are issued as and when the Dearness allowance has to be revised on the b.is of the cost of living index;

(ii) Direct the administering Ministries to compute the emoluments of persons who are to retire during the period of freezing, taking the correct amount of DA as admissible to receive and not what has been paid to him for computing gratuity and leave salary

(iii) The orders revising the rate of DA DR are to be issued in April, 2020, before September, 2020 and again in April, 2021.

No.21011/02/2015-Est(A-ll)-Part II

Government of India

Ministry of Personnel, Public Grievances and Pensions

Department of Personnel & Training

North Block, New Delhi

9th October, 2020

OFFICE MEMORANDUM

Subject : Extension of timelines for reporting / reviewing of part period of Annual Performance Assessment Report (APAR) of Group ‘A’, ‘B’ and ‘C’ officer of Central Civil Services during the current the year 2020-21, by officers retiring from 30.06.2020 to 31.10.2020.

The undersigned is directed to invite attention to Department of Personnel & A.R. O.M. No. 21011/1/77-Estt.(A) dated 30.01.1978 and this Department’s O.M. number 21011/1/93-Estt.(A) dated 14.01.1993 regarding recording of remarks by reporting and reviewing authority within one month after retirement (copies enclosed).

2. Due to unforeseen situation caused by COVID 19 pandemic, practical difficulty is being faced in recording the part period of APAR during the current year 2020-21 by the reporting / reviewing authority retiring on or after 30.06.2020. Accordingly, it has been decided, with the approval of the competent authority, that the reporting / reviewing authorities retiring from Government service during the period from 30.06.2020 to 31.10.2020, shall be allowed to record part period of the APAR for the current year 2020-21 of Group ‘A’, ‘B’ and ‘C’ officers of Central Civil Services, within 31.12.2020, in relaxation of the extant timelines for reporting and reviewing within one month after retirement. However, for reporting / reviewing authority retiring in November, 2020 or thereafter, the extant provisions as contained in O.Ms dated 30.01.1978 and 14.01.1993, mentioned at para 1 above, shall continue to be applicable.

3. The above relaxation is a one-time measure only.

No. 2/9/2017- Estt.(Pay-II)

Government of India

Ministry of Personnel, Public Grievances & Pensions

Department of Personnel & Training

North Block, New Delhi

Dated, 09th October, 2020.

OFFICE MEMORANDUM

Sub : Calculation of monthly contribution towards cost of Pension payable during foreign service – Reg.

The undersigned is directed to invite reference to this Department’s OM No. 2/34/2008-Estt (Pay-Il) dated 19th November, 2009 on the above subject and to say that according to this OM w.e.f. 01.01.2006, the pension contribution payable in respect of a Government employee during the active period of his foreign service shall be based on the existing basic pay (Pay in the Pay Band plus Grade Pay) of the post held by the Government servant at the time of proceeding on foreign service, and in case he receives Proforma promotion/financial up-gradation while on foreign service, on the basic pay (Pay in the Pay Band plus Grade Pay) fixed on such promotion/financial up-gradation.

2. Consequent upon implementation of the recommendations of the 7th CPC, the matter of issuing revised instructions on the above subject has been engaging the attention of the Government of India. The President is now pleased to decide that pension contribution payable in respect of a Government servant during the active period of his foreign service shall be based on the basic pay in the level (in Pay Matrix) of the post held by him/her at the time of proceeding on foreign service; and in case of grant of Proforma promotion/financial up-gradation while on foreign service, the same shall be based on basic pay in the Level (in Pay Matrix) fixed on such Proforma promotion / financial up-gradation.

3. In respect of Government employees covered by the NPS, during the active period of foreign service w.e.f. 01.01.2016, it has been decided to fix the monthly Pension contribution @ 24% of basic pay in the level (in Pay Matrix) of the post held by him/her at the time of proceeding on foreign service plus DA admissible on such basic pay (i.e. employee’s contribution @ 10%, employer’s contribution @ 10% and contribution by employer for gratuity @ 4%). However, consequent to revision of Government’s contribution for NPS from 10 % to 14% w.e.f. 01.04.20 19 vide Department of Financial Services Notification dated 31.01.2019, the monthly Pension contribution for Government employees covered by the NPS w.e.f. 01.04.2019 will be 28% of basic pay in the level (in Pay Matrix) plus DA of the post held by him/her, which will include employee’s contribution @ 10%, employer’s contribution @ 14%, and contribution by employer for gratuity @ 4%. In case of grant of Proforma promotion/financial up-gradation while on foreign service, the same shall be based on basic pay in the Level (in Pay Matrix) fixed on such Proforma promotion/financial up-gradation.

4. In respect of the employees covered under the Old Defined Benefit Pension Scheme, it has been decided to fix their rates of monthly contribution of pension during the active period of foreign service as 14% of basic pay in the level (in Pay Matrix) of the post held by him/her at the time of proceeding on foreign service plus DA admissible on such basic pay during foreign service w.e.f. 01.01.2016. The monthly contribution of pension during the active period of foreign service w.e.f. 01.04.2019 will be 18% of the basic pay in Pay Matrix of the post held by the officer at the time of proceeding on foreign service plus DA admissible on such basic pay. In case of grant of Proforma promotion/financial up-gradation while on foreign service, the same shall be based on basic pay in the Level (in Pay Matrix) fixed on such Proforma promotion/financial up-gradation.

5. It has also been decided that these pension contributions would be in addition to the leave salary contributions for the period of foreign service, in respect of both NPS employees and the employees under Old Defined Benefit Pension Scheme.

6. In case of employees covered under NPS, during the period of active foreign service, the borrowing organisation shall make its part of contribution mandatorily to the NPS Account of the employee.

7. This OM will be effective from 01.01.2016. In respect of persons who are already on foreign service as on 01.01.2016, the pension contribution will be calculated at the above rates on the revised pay as per 7th CPC from the date which they opt to come over to the revised pay structure after implementation of 7th CPC recommendations, in their parent cadres. For the earlier period, the pension contributions will be as per extant orders i.e. the order in force during period prior to 01.01.20 16 from time to time.

8. The modalities! mechanism of payment of pension contribution during the active period of foreign service in respect of NPS subscribers will be issued separately.

9. In their application to the persons belonging to Indian Audit and Accounts Department, these orders are issued under Article 148(5) of the Constitution and after consultation with the Comptroller & Auditor General of India.

10. Hindi version will follow.

(Rajeev Bahree)

Under Secretary to the Government of India

No.49014/7/2020-Estt.(C)

Government of India

Ministry of Personnel, PG & Pensions

Department of Personnel & Training

North Block, New Delhi

Dated: 7th October, 2020

OFFICE MEMORANDUM

Subject : Regularisation of qualified workers appointed against sanctioned posts – Uma Devi judgement – facts/clarification – reg.

The undersigned is directed to say that the instructions for Regularisation of qualified workers appointed against sanctioned posts in the light of Honible Supreme Court’s Judgement dated 10.04.2006 in case of Uma Devi were issued vide DoPT’s O.M. No. 49019/1/2006-Estt(C) dated 11.12.2006. The above instructions state that:

“in the case of Secretary State of Karnataka and Ors. Vs. Uma Devi it was directed that any public appointment has to be in terms of the Constitutional scheme. However, the Supreme Court in para 44 of the aforesaid judgement directed that the Union of India, the State Governments and their instrumentalities should take steps to regularize as a one time measure the services of such irregularly appointed, who are duly qualified persons in terms of the statutory recruitment rules for the post and who have worked for ten years or more in duly sanctioned posts but not under cover of orders of courts or tribunals.

Accordingly a copy of the above judgement is forwarded to all Ministries/Departments for implementation of the aforesaid direction of the Supreme Court.”

2. In this regard, various cases have been received in this department seeking clarifications regarding implementation of the above judgement. Therefore, it has been decided that further important aspects of the judgement dated 10.04.2006 may be enunciated for the purpose of clarity of the judgement. These important points as quoted from the judgement are reproduced below:

i. Equality of opportunity is the hallmark for public employment and it is in terms of the Constitutional scheme only (Para 1).

ii. The filling of vacancies cannot be done in a haphazard manner or based on patronage or other considerations (Para 2).

iii. The State is meant to be a model employer and can make appointments only in accordance with the rules framed under Article 309 of the Constitution (Para 5).

iv. Regularization is not and cannot be a mode of recruitment by any State within the meaning of Article 12 of the Constitution of India, or any body or authority governed by a statutory Act or the Rules framed thereunder. Regularization, furthermore, cannot give permanence to an employee whose services are ad hoc in nature. The fact that some persons had been working for a long time would not mean that they had acquired a right for regularization. (Para 27).

v. Any regular appointment made on a post under the State or Union without issuing advertisement inviting applications from eligible candidates and without holding a proper selection where all eligible candidates get a fair chance to compete would violate the guarantee enshrined under Article 16 of the Constitution (Para 30).

vi. If it is a contractual appointment, the appointment comes to an end at the end of the contract (Para 34).

vii. Regularization, if any already made, but not sub judice, need not be reopened based on this judgment, but there should be no further by-passing of the Constitutional requirement and regularizing or making permanent, those not duly appointed as per the Constitutional scheme (Para 44).

viii. In cases relating to service in the commercial taxes department, the High Court has directed that those engaged on daily wages, be paid wages equal to the salary and allowances that are being paid to the regular employees of their cadre in government service, with effect from the dates from which they were respectively appointed. The objection taken was to the direction for payment from the dates of engagement. We find that the High Court had clearly gone wrong in directing that these employees be paid salary equal to the salary and allowances that are being paid to the regular employees of their cadre in government service, with effect from the dates from which they were respectively engaged or appointed. It was not open to the High Court to impose such an obligation on the State when the very question before the High Court in the case was whether these employees were entitled to have equal pay for equal work so called and were entitled to any other benefit. They had also been engaged in the teeth of directions not to do so. We are, therefore, of the view that, at best, the Division Bench of the High Court should have directed that wages equal to the salary that are being paid to regular employees be paid to these daily wage employees with effect from the date of its judgment. Hence, that part of the direction of the Division Bench is modified and it is directed that these daily wage earners be paid wages equal to the salary at the lowest grade of employees of their cadre in the Commercial Taxes Department in government service, from the date of the judgment of the Division Bench of the High Court. Since, they are only daily wage earners, there would be no question of other allowances being paid to them (Para 46).

3. Additionally, it is also stated that vide the judgement of State of Karnataka Vs. M.L Kesari dated 03.08.2010, the Hon’ble Supreme Court had clarified some aspects of the Uma Devi judgement which are pertinent for proper understanding of the said judgement dated 10.04.2006. These aspects brought out in the M.L. Kesari judgement are reproduced as under:

i. The employee concerned should have worked for 10 years or more in duly sanctioned post without the benefit or protection of the interim order of any court or tribunal. In other words, the State Government or its instrumentality should have employed the employee and continued him in service voluntarily and continuously for more than ten years.

ii. The appointment of such employee should not be illegal, even if irregular. Where the appointments are not made or continued against sanctioned posts or where the persons appointed do not possess the prescribed minimum qualifications, the appointments will be considered to be illegal. But where the person employed possessed the prescribed qualifications and was working against sanctioned posts, but had been selected without undergoing the process of open competitive selection, such appointments are considered to be irregular.

iii. The employees who were entitled to be considered in terms of Para 53 of the decision in Umadevi, will not lose their right to be considered for regularization, merely because the one-time exercise was completed without considering their cases, or because the six month period mentioned in para 44 of Umadevi has expired. The one-time exercise should consider all daily-wage/adhoc1those employees who had put in 10 years of continuous service as on 10.4.2006 without availing the protection of any interim orders of courts or tribunals. If any employer had held the one-time exercise in terms of para 44 of Umadevi, but did not consider the cases of some employees who were entitled to the benefit of para 44 of Umadevi, the employer concerned should consider their cases also, as a continuation of the one-time exercise. The one time exercise will be concluded only when all the employees who are entitled to be considered in terms of Para 44 of Umadevi, are so considered.

4. It is also clarified that regularisation under Uma Devi judgement was only a one time exercise.

5. It is also emphasized that all concerned administrative authorities should take steps to effectively defend the Court cases on the basis of principles in the Uma Devi judgement and instructions of DoPT within the limitation period without giving any scope to the Courts to decide the cases against the Government on grounds of delay in filing its reply/appeal. Any laxity in the matter to comply with these instructions leading to adverse orders of the Courts shall be viewed seriously inviting disciplinary action in the matter.

(Umesh Kumar Bhatia)

Deputy Secretary to the Government of India

DoPT relaxes LTC facility for the government employees to travel by Air to visit J&K, Ladakh, North Eastern Region and Andaman & Nicobar Islands.

Travel relaxation has been extended up to 25th September 2022: Dr. Jitendra Singh

Government employees can avail LTC for these places in lieu of a hometown LTC

For ease of travel, employees can travel to these areas even by private Airlines

DoPT (Department of Personnel & Training) has issued orders relaxing the Leave Travel Concession (LTC) facility for the government employees to travel by Air to visit Jammu & Kashmir, Ladakh, North Eastern Region and Andaman & Nicobar Islands. Union Minister of State (Independent Charge) Development of North Eastern Region (DoNER), MoS PMO, Personnel, Public Grievances, Pensions, Atomic Energy and Space, Dr Jitendra Singh said that this relaxation has been extended up to 25th September 2022.

As a consequence, to this circular, Dr Jitendra Singh said that an entitled government official can avail LTC for visiting Jammu & Kashmir, North Eastern Region, Ladakh and Andaman & Nicobar in lieu of a hometown LTC.

In addition, the facility of Air journey to non-entitled government servants will be available for visiting Jammu & Kashmir, North Eastern Region, Ladakh and Andaman &Nicobar Islands. As a further convenience, ease of travel permission is also being granted to undertake journey to these areas by private Airlines, whereas normally a government servant is expected to travel by the state owned Air India, he added.

Pertinent to mention that in relaxation to Central Civil Services (LTC) Rules 1988, the scheme allowing government servants to travel by Air to visit Union Territory of Jammu & Kashmir, Union Territory of Ladakh, the North Eastern States and Union Territory of Andaman & Nicobar Islands has been extended for a period of two years till 25th September 2022.

Describing this as a huge and an exclusive facility for the government employees, Dr Jitendra Singh said that all eligible government servants may avail LTC to visit Jammu & Kashmir or North East or any of these mentioned areas against the conversion of their one Home Town LTC in a four-year block. However, the government servants whose hometown and place of posting is the same, are not allowed this conversion. He said, such government servants who are not otherwise entitled to travel by Air will also be allowed to travel by Air, under the norms of this scheme, in Economy class by any Airlines, subject to the maximum fare limit of LTC-80 scheme.

Ever since the Modi government took over in 2014, said Dr Jitendra Singh, it has been the direction of Prime Minister Narendra Modi to give priority to the far flung and difficult regions, and do whatever possible for ease of living and ease of governance in these areas.

F.No.11013/9/2014-Estt.A.III

Government of India

Ministry of Personnel, Public Grievances and Pensions

(Department of Personnel and Training)

***

North Block, New Delhi

Dated the 7th October, 2020

OFFICE MEMORANDUM

Subject : Preventive measures to contain the spread of Novel Coronavirus (COVID-19) – Attendance of Central Government officials regarding.

The undersigned is directed to refer to OM of even number dated the 5th June, 2020 reiterating, inter alia, the instructions/advisory issued vide OMs dated 17.3.2020, 18.5.2020 and 19.5.2020 for well-being of Government employees and regulating attendance of Central Government employees in offices with staggered timings. The matter has now been reviewed and it has been decided as under: –

(a) The Government servants at the level of Under Secretary and above to attend offices on all working days.

(b) As regards Government servants below the level of Under Secretary, at least 50% of attendance is to be ensured. The Heads of Department may mandate attendance of more than 50%, if required in public interest, while strictly ensuring that social distancing is maintained under all circumstances.

(c) The officers/staff shall follow staggered timings to avoid over-crowding in offices/work places as indicated below.

9.00 am. to 5.30 p.m.

10.00 a.m. to 6.30 p.m.

(d) All officers/staff residing in the containment zone shall be exempted from coming to offices till the containment zone is denotified.

(e) Those officers/staff who are not attending office shall work from home and they should be available on telephone and electronic means of communication at all times.

(f) Persons with Disabilities and Pregnant women employees shall continue to work from home till further orders.

(g) Heads of Departments shall ensure that the National Directives for the Covid-19 management, which include instructions issued for regular sanitization/cleaning of working places, maintenance of social distancing norms, wearing of masks etc. are strictly complied with. It may also be strictly ensured that there is no crowding in the corridors.

(h) Meetings, as far as possible, shall be conducted on video-conferencing and personal meetings with visitors, unless absolutely necessary in public interest, are to be avoided.

2. The above instructions shall be in force with immediate effect until further orders. Biometric attendance shall continue to be suspended and physical attendance registers shall be maintained until further orders. The Heads of the Department may kindly ensure strict implementation of these instructions.

(Umesh Kumar Bhatia)

Deputy Secretary to the Govt. of India

F.No. 14(02)/2019/D(Pen/Pol)

Government of India

Ministry of Defence

Department of Ex-Servicemen Welfare

D(Pension/Policy)

Room No.222, ‘B’ Wing,

Sena Bhawan, New Delhi-110011.

Dated: 5th October, 2020

To,

The Chief of the Army Staff

The Chief of the Naval Staff

The Chief of the Air Staff

Sub : Revision of Regulation relating to rate of Family Pension (Normal rate & Enhanced rate) of Pension Regulation for the Army, Part-I (2008) in the line of amendment done in Sub Rule (3) of Rule 54 of CCS Pension Rule, 1972 by DoP&PW-reg.

Sir,

The undersigned is directed to refer to the provision of Note 3 (i) & (ii) below Army Instruction 51/80 and Regulation 64 (b) in Pension Regulation for Army, Part-I (2008) under which the minimum of 7 years of continuous qualifying service is required for grant of enhanced rate of Family Pension for the Armed Forces personnel.

2. Consequent upon issue of Gazette Notification No. 550 dated 19.09.2019 of the Ministry of Personnel, Public Grievances & Pensions, Department of Pension and Pensioners’ Welfare (DoP&PW), the condition of minimum requirement of 7 years of continuous service for grant of enhanced rate of Ordinary Family Pension in the sub rule (3)(a) & (b) of Rule 54 of CCS Pension Rule, 1972 has been deleted w.e.f 1st October, 2019 and now Government servants who died in service/invalided out even with less than 7 years of qualifying service shall be eligible for enhanced rate of Family Pension. This notification also has a provision where a Government servant who died within ten years before the 1st day of October 2019 without completing continuous service of seven years, his family shall be eligible for family pension at enhanced rates in accordance with sub rule (3) with effect from the 1st day of October 2019, subject to fulfillment of other conditions for grant of family pension.

3. Now, the President is pleased to decide that the same provision shall be extended to Armed Forces Personnel also. Accordingly, the clause “after having rendered not less than 7 years continuous qualifying service” of Regulation 64{b) of Pension Regulations for the Army, Part-I (2008) stands deleted w.e.f. 01.10.2019.

4. It has also been decided that where an Armed Forces Personnel died within ten years before the 1st October, 2019 without completing continuous service of seven years, his family shall be eligible for ordinary family pension at enhanced rate as per Regulations 64(b) of Pension Regulations for the Army Part-I(2008) with effect from the 1st October 2019 subject to fulfillment of other conditions for grant of Ordinary Family Pension.

5. Further, the provision of Army Instruction No. 51/1980 would stand modified upto this extent w.e.f. 01.10.2019. The regulation and their instructions for grant of Ordinary Family Pension in Navy and Air Force shall also be amended accordingly.

6. This issues with the concurrence of the Finance Division of this Ministry vide their ID No. 10(02)/2020/FIN/PEN dated 23.09.2020.