AICPIN for October 2022: Expected DA from Jan 2023

Consumer Price Index for Industrial Workers for October 2022 released

All-India CPI-IW for October, 2022 increased by 1.2 points and stood at 132.5

The Labour Bureau, an attached office of the Ministry Labour and Employment, has been compiling Consumer Price Index for Industrial Workers every month on the basis of retail prices collected from 317 markets spread over 88 industrially important centres in the country. The index is compiled for 88 centres and All-India and is released on the last working day of succeeding month. The index for the month of October, 2022 was released today

The All-India CPI-IW for October, 2022 increased by 1.2 points and stood at 132.5 (one hundred thirty two point five). On 1-month percentage change, it increased by 0.91 per cent with respect to previous month compared to an increase of 1.30 per cent recorded between corresponding months a year ago.

Also Check

The maximum upward pressure in current index came from Food & Beverages group contributing 0.76 percentage points to the total change. At item level, Rice, Wheat, Wheat Atta, Buffalo Milk, Poultry/Chicken, Cauliflower, Cabbage, Onion, Potato, Tomato, Peas, Chillies dry, Biscuits, Vada, Idli, Dosa, Cooked Meals, Tea cup, Doctor’s fee etc. are responsible for the rise in index. However, this increase was largely checked by Apple, Banana, Fish fresh, Palm Oil, Mustard oil, Cotton seed Oil, Sunflower Oil, Chillies Green, Brinjal, Orange, French Bean, Electricity Domestic etc. putting downward pressure on the index.

At centre level, Ludhiana recorded a maximum increase of 3.6 points. Among others, 4 centres recorded increase between 3 to 3.4 points, 14 centres between 2 to 2.9 points, 29 centres between 1 to 1.9 points and 25 centres between 0.1 to 0.9 points. On the contrary, Doom-Dooma Tinsukia and Haldia recorded a maximum decrease of 1.3 points each. Among others, 2 centers recorded decrease between 1 to 1.2 points, 8 centres between 0.1 to 0.9 points. Rest of three centers index remained stationary.

Year-on-year inflation for the month stood at 6.08 per cent compared to 6.49 per cent for the previous month and 4.52 per cent during the corresponding month a year before. Similarly, Food inflation stood at 6.52 per cent against 7.76 per cent of the previous month and 2.20 per cent during the corresponding month a year ago.

Y-o-Y Inflation based on CPI-IW (Food and General)

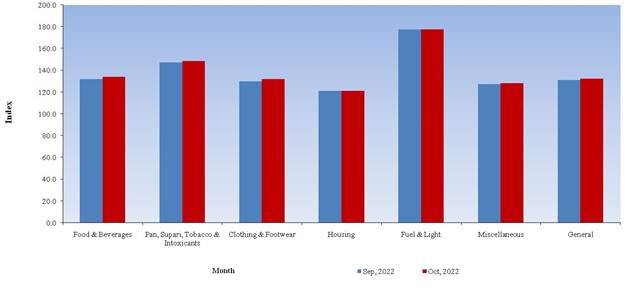

All-India Group-wise CPI-IW for September, 2022 and October, 2022

| Sr. No. | Groups | September, 2022 | October, 2022 |

| I | Food & Beverages | 131.9 | 133.9 |

| II | Pan, Supari, Tobacco & Intoxicants | 147.3 | 148.5 |

| III | Clothing & Footwear | 129.7 | 131.9 |

| IV | Housing | 121.0 | 121.0 |

| V | Fuel & Light | 177.8 | 177.8 |

| VI | Miscellaneous | 127.5 | 128.4 |

| General Index | 131.3 | 132.5 |

CPI-IW: Groups Indices

The next issue of CPI-IW for the month of November, 2022 will be released on Friday, 30th December, 2022. The same will also be available on the office website www.labourbureaunew.gov.in.

Follow us on Telegram Channel, Twitter and Facebook for all the latest updates