Grant of Fixed Medical Allowance to Railway pensioners – change in option: Railway Board

GOVERNMENT OF INDIA MINISTRY OF RAILWAYS (Railway Board)

S.No. PC-VII/200 No. PC-V/2016/A/Med/I(FMA)(E)

RBE No. 137/2022 New Delhi, dated 27-10-2022

The General Managers co All Indian Railways and PUs, (as per mailing list)

Sub: Grant of Fixed Medical Allowance to Railway pensioners/family pensioners – change in option.

In terms of Railway Board’s letter No. PC-V/98/I/7/1/1 dated 15-7-2002 (RBE No. 107/2002), the Railway pensioners/family pensioners eligible to opt for FMA had been provided, once in a life time, an opportunity to change their option to avail the benefit of FMA or otherwise on furnishing proof of change in residence. The issue of allowing this one time opportunity to change option for FMA/OPD facility had been under consideration with DoP&PW for quite some time. It has now been decided that the Railway pensioners/family pensioners residing beyond 2.5 kms from Railway Hospital/Health Unit and eligible for RELHS shall be allowed opportunity to avail change in option, once in a life time, from FMA to OPD or a vice versa without linkage to change in residence.

DA for Bank Employees from Nov 2022 to Jan 2023, IBA Order

Indian Banks’ Association

HR & Industrial Relations

HR&IR/MBR/76/D/2022-23/11592 November 1, 2022

All Members of the Association (Designated Officers)

Dear Sir/ Madam,

Dearness Allowance for Workmen and Officer Employees in banks for the months of November, December 2022 and January 2023 under XI BPS/ Joint Note dated 11.11.2020

The confirmed All India Average Consumer Price Index Numbers for Industrial Workers (Base 1960=100) for the quarter ended September 2022 as published by Govt. of India in its website Labour Bureau are as follows:-

July 2022

8539.44

August 2022

8559.16

September 2022

8631.48

The average CPI of the above is 8576.69 and accordingly the number of DA slabs are 556 (8576 — 6352= 2224/4= 556 Slabs). The last quarterly Payment of DA was at 526 Slabs. Hence, there is an increase in DA slabs of ‘30’ i.e. 556 Slabs for payment of DA for the months November, December 2022 and January 2023.

In terms of clause 7 of the 11th Bipartite Settlement dated 11.11.2020 and clause 3 of the Joint Note dated 11.11.2020, the rate of Dearness Allowance payable to Workmen and Officer employees for the months of November, December 2022 and January 2023 shall be 38.92% of ‘pay’. While arriving at dearness allowance payable, decimals from third place may please be ignored.

5th CPC Dearness Relief from July 2022 to CPF beneficiaries in receipt of basic ex-gratia payment

No. 42/07/2022-P&PW(D) Government of India Ministry of Personnel, Public Grievances & Pensions Department of Pension & Pensioners’ Welfare

3rd Floor, Lok Nayak Bhavan, Khan Market, New Delhi – 110003 Dated 31st Oct, 2022

OFFICE MEMORANDUM

Sub:- Grant of Dearness Relief in the 5th CPC series effective from 01.07.2022 to CPF beneficiaries in receipt of basic ex-gratia payment – reg

The undersigned is directed to refer to this Department’s OM of even no. dated 11.05.2022 and to say that the President is pleased to decide that the Dearness Relief admissible to the CPF beneficiaries in receipt of basic ex-gratia payment in the 5th CPC series shall be enhanced w.e.f 01.07.2022 in the following manner :-

(i) The surviving CPF beneficiaries who have retired from service between the period 18.11.1960 and 31.12.1985, and are entitled to basic ex-gratia @ Rs.3000, Rs.1000, Rs.750 & Rs.650 for Group A, B, C & D respectively w.e.f 4th June,2013 vide OM No. 1/10/2012-P&PW(E) dtd. 27th June, 2013 shall now be entitled to enhanced Dearness Relief from 381% of the basic ex-gratia to 396% of the basic ex-gratia w.e.f 01.07.2022.

(ii) The following categories of CPF beneficiaries shall be entitled to enhanced Dearness Relief from 373% of the basic ex-gratia to 388% of the basic ex-gratia w.e.f 01.07.2022:-

(a) The widows and eligible dependent children of the deceased CPF beneficiary who had retired from service prior to 01.01.1986 or who had died while in service prior to 01.01.1986 and are entitled to revised ex-gratia @ Rs.645/-p.m w.e.f 04 June, 2013 vide OM No 1/10/2012-P&PW(E) dated 27th June,2013.

(b) Central Government employees who had retired on CPF benefits before 18.11.1960 and are in receipt of Ex-gratia payment of Rs. 654/-, Rs.659/-, Rs.703/- and Rs.965/-.

2. Payment of DR involving a fraction of a rupee shall be rounded off to the next higher rupee.

3. It will be the responsibility of the pension disbursing authorities, including the nationalized banks, etc. to calculate the quantum of DR payable in each individual case.

4. In so far as the persons serving in Indian Audit and Accounts Department are concerned, these orders are issued in consultation with the Comptroller and Auditor General of India, as mandated under Article 148(5) of the Constitution of India.

5. This issues in pursuance of Ministry of Finance, Department of Expenditure’s OM No. 1/3(2)/2008-E.II(B) dated 12th October, 2022.

6. Hindi version will follow.

(Charanjit Taneja) Under Secretary to the Government of India

Admissibility of Dearness Relief on additional pension/additional compassionate allowance and additional family pension

No. 42/15/2022-P&PW(D)/8 Government of India Ministry of Personnel, P.G. & Pensions Department of Pension & Pensioners’ Welfare

3rd Floor, Lok Nayak Bhawan, Khan Market, New Delhi-110003 Date:- 31st Oct, 2022

OFFICE MEMORANDUM

Sub:- Admissibility of Dearness Relief on additional pension/additional compassionate allowance and additional family pension – Clarification regarding

In accordance with Rule 52 of CCS (Pension) Rules, 2021, Dearness Relief on Pension and Family Pension against price rise is granted to Pensioners including the persons drawing compassionate allowance under Rule 41 and Family Pensioners at such rates and subject to such conditions as the Central Government may specify from time to time.

2. References/Representations have been received in this Department seeking clarification whether the Dearness Relief is also payable on additional pension/additional compassionate allowance and additional family pension.

3. It is clarified that the terms pension/compassionate allowance and family pension refer to in Rule 52 of the CCS (Pension) Rules, 2021 also include additional pension/additional compassionate allowance and additional family pension.

4. Reference is also invited to this Department’s OM No. 38/37/08-P&PW(A).pt.I dated 03.10.2008 wherein it was clarified that Dearness Relief will also be admissible to additional quantum of pension available to the old pensioners in accordance with the orders issued from time to time.

5. The above clarification may be brought to the notice of the personnel dealing with the pensionary benefits for strict implementation.

(Charanjit Taneja) Under Secretary

All Ministries/Departments of the Government of India

Interest on delayed payment of commuted value of pension: DOPPW Clarification

No. 42/15/2022-P&PW(D)/7 Government of India Ministry of Personnel, P.G. & Pensions Department of Pension & Pensioners’ Welfare

3 Floor, Lok Nayak Bhawan, Khan Market, New Delhi-1 10003 Date:- 31st Oct, 2022

OFFICE MEMORANDUM

Sub:- Interest on delayed payment of commuted value of pension – Clarification regarding

In accordance with Rule 5 of CCS (Commutation of Pension) Rules, 1981, a Government servant can commute for a lump-sum payment of an amount not exceeding 40 per cent of his pension. In cases where a Government servant has applied for commutation of pension before superannuation, the commuted value of pension is to be paid at the time of retirement. In other cases, the commuted value of pension should be paid as soon as possible after it has become absolute

2. References are received in this Department seeking clarification whether any interest is required to be paid to the retired Government servant in cases where there is a delay in payment of commuted value of pension after it has become absolute.

3. It is clarified that in accordance with Rule 6 of the CCS (Commutation of Pension) Rules, 1981, in cases where the commuted value of pension is paid after retirement, the reduction of the amount of commuted pension from the monthly pension becomes operative from the date on which the Commuted value of pension is paid. As per Rule 10A of CCS(Commutation of Pension) Rules, the commuted amount of the pension is restored on completion of fifteen years from the date the reduction of pension on account of commutation becomes operative in accordance with Rule 6. Since the pensioner continues to receive full pension till the date of payment of commuted value of pension, the question of payment of any interest on delayed payment of commutation of pension does not arise.

4. The above clarification may be brought to the notice of the personnel dealing with the pensionary benefits in the Ministry/Department and attached/subordinate offices thereunder, for strict implementation. The above provisions of the rules may also be suitably incorporated in the replies to be filed in the court cases on this issue.

(Charanjit Taneja) Under Secretary

l. All Ministries/Departments of the Government of India 2. C&AG of India, UPSC, etc.

Commutation of pension on more than one occasion: DOPPW Clarification

No. 42/15/2022-P&PW(D)/6 Government of India Ministry of Personnel, P.G. & Pensions Department of Pension & Pensioners’ Welfare

3rd Floor, Lok Nayak Bhawan, Khan Market, New Delhi – 110003 Date:- 31st Oct, 2022

OFFICE MEMORANDUM

Sub:- Commutation of pension on more than one occasion – Clarification regarding

In accordance with Rule 5 of CCS (Commutation of Pension) Rules, 1981, a Government servant can commute for a lump-sum payment of an amount not exceeding 40 per cent of his basic pension.

2. References/representations have been received in this Department seeking clarification whether it is permissible for a person, who has commuted a percentage of his basic pension which is less than 40% of his basic pension, to commute a percentage of basic pension on a second or subsequent occasion within the overall maximum limit of 40%.

3. As per Rule 10 of CCS (Commutation of Pension) Rules, 1981, an applicant who has commuted a percentage of his final pension and after commutation his pension has been revised and enhanced retrospectively as a result of Government’s decision, the applicant shall be paid the difference between the commuted value determined with reference to enhanced pension and the commuted value already authorized. For the payment of difference, the applicant shall not be required to apply afresh. This Department’s OM No. 42/14/2016-P&PW (G) dated 24.10.2016 provides that those pensioners who retired from 01.01.2016 till 04.08.2016, i.e. the date of issue of orders for revised pay/pension based on the recommendations of the 7th CPC, may be given an option, in relaxation of Rule 10 of CCS (Commutation of Pension), Rules, 1981, not to commute the pension which has become additionally commutable on revision of pay/pension on implementation of recommendations of the 7th CPC.

4. There is, however, no provision in the Central Civil Services (Commutation of Pension) Rules, 1981 for commutation of a percentage of basic pension on a second or subsequent occasion within the overall maximum limit of 40%, if the pensioner had originally commuted a percentage of his basic pension which was less than 40% of his basic pension.

5. The above clarification may be brought to the notice of the personnel dealing with the pensionary benefits in the Ministry/Department and attached/subordinate offices thereunder, for strict implementation.

(Charanjit Taneja) Under Secretary

All Ministries/Departments of the Government of India.

Central Civil Services (Classification, Control and Appeal) Amendment Rules 2022: Gazette Notification

MINISTRY OF PERSONNEL, PUBLIC GRIEVANCES AND PENSIONS (Department of Personnel and Training) New Delhi, the 19th October, 2022

G.S.R. 156.—In exercise of the powers conferred by proviso to article 309 and clause (5) of article 148 of the Constitution, and after consultation with the Comptroller and Auditor General of India in relation to persons serving in the Indian Audit and Accounts Department, the President hereby makes the following rules further to amend the Central Civil Services (Classification, Control and Appeal) Rules, 1965, namely: —

1. Short title and commencement:- (1) These rules may be called the Central Civil Services (Classification, Control and Appeal) Amendment Rules, 2022.

(2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Central Civil Services (Classification, Control and Appeal) Rules, 1965, in rule 10, in sub-rule (7), for the proviso, the following provisos shall be substituted, namely: —

“Provided that no such review of suspension shall be necessary in the case of deemed suspension under sub-rule (2), if the Government servant continues to be under detention and in such case the ninety days’ period shall be computed from the date the Government servant detained in custody is released from detention or the date on which the fact of his release from detention is intimated to his appointing authority, whichever is later:

Provided further that in a case where no charge sheet is issued under these rules, the total period under suspension or deemed suspension, as the case may be, including any extended period in terms of sub-rule (6) shall not exceed,—

(a) two hundred seventy days from the date of order of suspension, if the Government servant is placed under suspension in terms of clause (a) of sub-rule (1); or

(b) two years from the date of order of suspension, if the Government servant is placed under suspension in terms of clause (aa) or clause (b) of sub-rule (1) as the case may be; or

(c) two years from the date the Government servant detained in custody is released or the date on which the fact of his release from detention is intimated to his appointing authority, whichever is later, in the case of deemed suspension under sub-rule (2).”.

[F. No. 11012/04/2016-Estt.A-III] MANOJ KUMAR DWIVEDI, Jt. Secy.

Note: The principal rules were published in the Gazette of India vide notification number S.O. 3703, dated the 20th November, 1965 and last amended vide notification number G.S.R. 125 (E) dated the 18th February, 2021 published in the Gazette of India.

Review of CSS Officers under FR 56 (j) and Rule 48 of CSS (Pension) Rules, 1972 – Request for information

No.21/1/2022-CS.I(U) Government of India Ministry of Personnel, Public Grievances & Pensions (Department of Personnel & Training)

Lok Nayak Bhawan, New Delhi-110003 Dated 31st October, 2022

OFFICE MEMORANDUM

Subject: Review of CSS Officers (Under Secretary) under FR 56 (j) and Rule 48 of CSS (Pension) Rules, 1972 – Request for information – regarding

The undersigned is directed to refer to the subject mentioned above and to state that information/ complete inputs is required for review under FR 56(j) and Rule 48 of CSS (Pension) Rules 1972 in DoP&T in respect of Under Secretary level officer of CSS of Ministries/ Departments, who have crossed the age of 50 years on 01.07.2022.

2. The above-mentioned data/inputs may be provided in the 15 columns prescribed proforma (copy enclosed), in hard copy or through email address at [email protected]. The soft copy of the inputs may also be sent at the said email address in the excel format only, as per the proforma, not in any other format like pdf, word etc.

3. Incomplete information: It is stated that on previous occasions, some of the Ministries/Departments did not furnish the complete information in the format prescribed by this Department. It may, therefore, be ensured that no column is left blank. For example, against the column ‘total leaves availed during the past five years’, entries are required to be made therein.

4. It is also stated that DoPT being the custodian of APARs of Group-I and above level CSS Officers, provides inputs from APARs to the Review Committee for their consideration. The inputs sought from the Ministries/Departments in the 15 columns prescribed proforma are over and above what is recorded in the APARs and hence it may be ensured that these columns are not left blank. It may also be ensured that the inputs of the Ministry/Department may be communicated at an appropriate level, with the name, designation, email-id and telephone number of the officer clearly indicated.

Encl: As above

(Sunil Kumar) Under Secretary to the Govt. of India

AICPIN for September 2022: Expected DA from Jan 2023

Consumer Price Index for Industrial Workers (2016=100) – September, 2022

TheLabour Bureau, an attached office of the Ministry of Labour & Employment, has been compiling Consumer Price Index for Industrial Workers every month on the basis of retail prices collected from 317 markets spread over 88 industrially important centres in the country. The index is compiled for 88 centres and All-India and is released on the last working day of succeeding month.

The All-India CPI-IW for September, 2022 increased by 1.1 points and stood at 131.3 (one hundred thirty-one point three). On 1-month percentage change, it increased by 0.84 per cent with respect to previous month compared to an increase of 0.24 per cent recorded between corresponding months a year ago.

The maximum upward pressure in current index came from Food & Beverages group contributing 0.68 percentage points to the total change. At item level Rice, Wheat Atta, Buffalo Milk, Dairy milk, Poultry/Chicken, Carrot, Cauliflower, Green Coriander leaves, Onion, Potato, Tomato, Vada, Idli, Dosa etc. are responsible for the rise in index. However, this increase was largely checked by Fish fresh, Palm Oil, Mustard oil, Sunflower oil, Soyabeen oil, Apple, Asafoetida, Orange, Gourd (Lauki) etc. putting downward pressure on the index.

At centre level, Bhavnagar recorded a maximum increase of 4.5 points. Among others, 6 centres recorded increase between 3 to 3.9 points, 10 centres between 2 to 2.9 points, 24 centres between 1 to 1.9 points and 30 centres between 0.1 to 0.9 points. On the contrary, Chindwara, Ahmedabad and Shilong recorded a maximum decrease of 0.6 points each. Among others, 8 centers recorded decrease between 0.1 to 0.9 points. Rest of six centers index remained stationary.

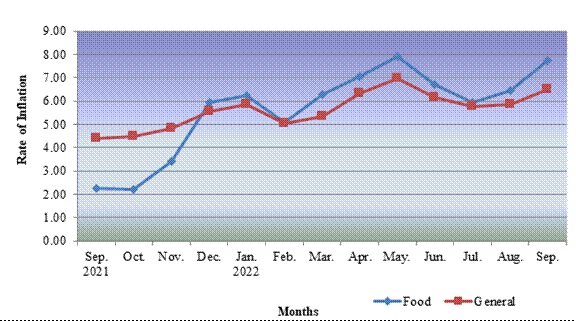

Year-on-year inflation for the month stood at 6.49 per cent compared to 5.85 per cent for the previous month and 4.40 per cent during the corresponding month a year before. Similarly, Food inflation stood at 7.76 per cent against 6.46 per cent of the previous month and 2.26per cent during the corresponding month a year ago.

Y-o-Y Inflation based on CPI-IW (Food and General)

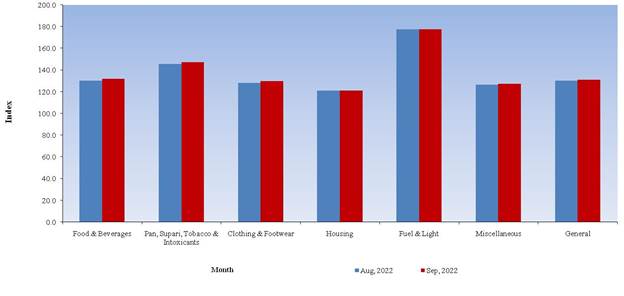

All-India Group-wise CPI-IW for August, 2022 and September, 2022

Sr. No.

Groups

August, 2022

September, 2022

I

Food & Beverages

130.2

131.9

II

Pan, Supari, Tobacco & Intoxicants

145.7

147.3

III

Clothing & Footwear

128.2

129.7

IV

Housing

121.0

121.0

V

Fuel & Light

177.4

177.8

VI

Miscellaneous

126.6

127.5

General Index

130.2

131.3

CPI-IW: Groups Indices

The next issue of CPI-IW for the month of October, 2022 will be released on Wednesday, 30th November, 2022. It will be available on the office website www.labourbureaunew.gov.in.

Entitlement for family on death of a Central Government servant covered under National Pension System

No. – 57/03/2022-P&PW(B)/8361 (1) Government of India Ministry of Personnel, Public Grievances and Pensions Department of Pension and Pensioners’ Welfare ***

3rd Floor, Lok Nayak Bhavan, Khan Market, New Delhi, Dated the 28th October, 2022

OFFICE MEMORANDUM

Subject: Entitlement for family on death of a Central Government servant covered under National Pension System – reg.

The undersigned is directed to say that Department of Pension and Pensioners’ Welfare has notified the Central Civil Services (Implementation of National Pension System) Rules, 2021 and Central Civil Services (Payment of Gratuity under National Pension System) Rules, 2021 which are applicable from the date of its publication in the Official Gazette, to govern service related matters and for grant of gratuity respectively to Central Government civil employees covered under National Pension System.

2. Rule 20 of the Central Civil Services (Implementation of NPS) Rules, 2021 provides for the entitlement of family members on death of a Central Government covered under National Pension System. As per rule 20, on death of a Subscriber, who had exercised option or in whose case the default option under rule 10 of the CCS(Implementation of NPS) Rules, 2021 is for availing benefits under the Central Civil Services (Pension) Rules, 1972 or Central Civil Services (Extraordinary Pension) Rules , further action will be taken by the Head of Office for disbursement of benefits in accordance with the Central Civil Services (Pension) Rules. However, if the death is attributable to Government service, further action will be taken by the Head of Office for disbursement of benefits in accordance with the Central Civil Services (Extraordinary Pension) Rules subject to fulfillment of all the conditions for grant of benefits under those rules.

3. If on death of the Subscriber, benefits are payable to the family under the Central Civil Services (Extraordinary Pension) Rules or the Central Civil Services (Pension) Rules, the Government contribution and returns thereon in the accumulated pension corpus of the Subscriber shall be transferred to Government account. The remaining accumulated pension corpus shall be paid in lump sum to the person(s) in whose favour a nomination has been made under the Pension Fund Regulatory and Development Authority (Exits and Withdrawals under National Pension System) Regulations, 2015. If there 1s no such nomination or if the nomination made does not subsist, the amount of remaining accumulated pension corpus shall be paid to the legal heir(s).

4. In the case of death of a Subscriber who had exercised option or in whose case the default option under rule 10 of the CCS(Implementation of NPS) Rules, 2021 is for availing benefits under the National Pension System, such benefits may be granted in accordance with the Pension Fund Regulatory and Development Authority (Exits and Withdrawals under National Pension System) Regulations, 2015.

5. In the event of death of Government employees covered under NPS during service, and in whose case benefits from accumulated pension corpus under NPS have been availed, family member of such deceased Government employee would also be eligible for death gratuity in accordance with rule 22 of the Central Civil Services (Payment of Gratuity under NPS) Rules, 2021. The rates provided in the rules for death gratuity is as under:

Sl. No.

Length of qualifying service

Rate of death gratuity

(i)

Less than one year

Two times of emoluments.

(ii)

Once year or more but less than five years

Six times of emoluments

(iii)

Five years or more but less than eleven years

Twelve times of emoluments

(iv)

Eleven years or more but less than twenty years re

Twenty times of emoluments

(v)

Twenty years or more

Half of emoluments for every completed six monthly period of qualifying service subject to a maximum of thirty three times of emoluments:

The maximum amount of death gratuity payable under this rule shall in no case exceed twenty lakh rupees.

6. All Ministries/Departments are requested that the above provisions regarding entitlement in respect to Central Government employees covered under National Pension System may be brought to the notice of the Government servants covered under NPS and personnel dealing with the pensionary benefits in the Ministry/Department and attached/subordinate offices thereunder, for strict implementation.

(S. Chakrabarti) Under Secretary to the Government of India

To All Ministries/Departments/Organisations, (As per standard list)